From Hidden Premium Discounts to Everyday Mobility Rewards: How RideUSD Could Reshape Auto Insurance Incentives

For decades, auto insurance companies have tried to reward “good drivers” through safe driver discounts, accident forgiveness, and loyalty programs. But ask most customers if they feel rewarded for years of safe driving, and the answer is usually the same: Not really.

That’s because traditional insurance rewards are mostly invisible. Drivers may go 5, 10, or even 20 years without an accident, yet the benefit often feels limited to simply not getting penalized. Then after a single claim or rate increase, years of loyalty can suddenly feel erased.

The problem isn’t just pricing. It’s the reward model itself.

The Problem with Traditional Insurance Rewards

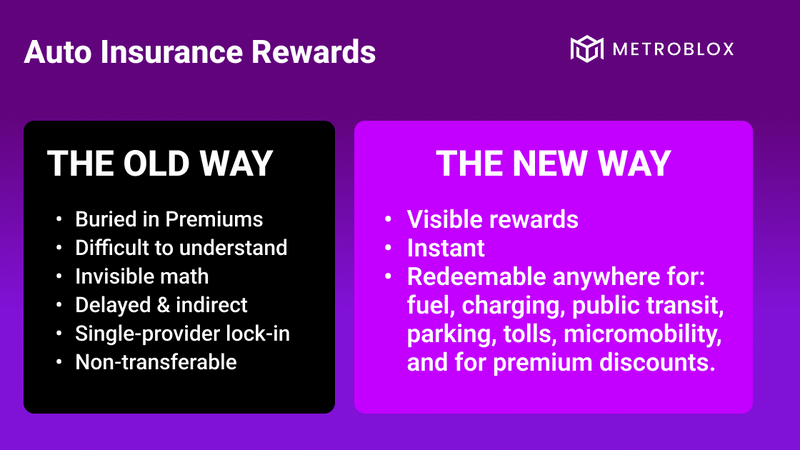

Most insurance incentives are:

-

Buried inside premium calculations

-

Difficult for customers to understand

-

Locked inside a single insurance provider

-

Delayed or indirect

-

Non-transferable

A customer might technically receive a “safe driver discount,” but it doesn’t feel tangible in everyday life.

Consumers today are used to rewards systems that are:

-

Instant

-

Visible

-

Flexible

-

Redeemable anywhere

Insurance has largely failed to evolve in that direction.

A Different Approach: Mobility Rewards Instead of Insurance Discounts

What if safe driving behavior generated real-world mobility rewards that drivers could actually use across the transportation ecosystem?

This is where digital settlement infrastructure like RideUSD and Universal Ride Token (URT) create a new model.

Instead of only reducing premiums behind the scenes, insurers could issue:

-

RideUSD for verified safe driving

-

URT rewards for low-risk behavior, low mileage, EV adoption, or accident-free periods

Those rewards could then be redeemed throughout the mobility ecosystem, including:

-

Gas stations

-

EV charging

-

Public transit

-

Parking

-

Bike share

-

Tolls

-

Rideshare

-

Mobility subscriptions

Rather than rewarding drivers with invisible math on an insurance statement, rewards become usable transportation value.

Why This Changes Consumer Psychology

Traditional insurance rewards feel passive. Mobility rewards feel immediate.

For example:

-

Safe driver for 12 months → receive mobility credits

-

Low-risk driving score → earn URT monthly

-

Reduced mileage → unlock transit or parking incentives

Now the reward is no longer abstract. Drivers can actually see the value and use it in daily life. This creates a stronger behavioral loop:

-

Safer driving

-

Lower claims

-

Lower insurance losses

-

Better customer engagement

-

More transportation spending retained inside the ecosystem

Universal Rewards Are More Valuable Than Closed Rewards

One of the biggest limitations of traditional insurance programs is that rewards are usually closed-loop:

-

Discounts only apply to future premiums

-

Points expire

-

Benefits stay trapped inside one company

URT introduces the idea of universal mobility rewards. Instead of a reward tied to one insurer or one app, drivers could redeem rewards across participating transportation providers.

A commuter could: Earn rewards through safe driving and:

-

Redeem them at a train station

-

Use them for parking downtown

-

Apply them toward EV charging

-

Spend them on bike share or tolls

This creates a much broader and more engaging transportation economy.

Why This Matters for Insurers

Insurance companies spend billions trying to:

-

Reduce claims

-

Improve retention

-

Increase customer engagement

-

Encourage safer behavior

But premium discounts alone are becoming less effective as a customer engagement strategy.

Programmable mobility rewards create a new opportunity:

-

Reward behavior in real time

-

Create partnerships across mobility networks

-

Improve customer loyalty

-

Incentivize lower-risk transportation patterns

-

Connect insurance to the broader mobility ecosystem

Instead of acting only as a claims payer, insurers could become active participants in transportation incentives.

The Future of Insurance May Be Mobility-Centric

Transportation is becoming increasingly connected:

-

Vehicles

-

Parking

-

Transit

-

EV charging

-

Micromobility

-

Digital payments

-

Identity

-

Incentives

Insurance rewards should evolve with it.

The future likely won’t be built around invisible discounts buried in annual policy renewals. It will be built around interoperable, real-time rewards that consumers can actually use in their daily transportation lives.

RideUSD and URT represent a new model for mobility and insurance incentives - one built around real-world utility instead of invisible discounts.

-

Instant settlement with RideUSD

-

Programmable rewards tied to safe driving and mobility behavior

-

Universal mobility rewards through URT

-

Redeemable across parking, transit, fuel, EV charging, tolls, bike share, and more

-

Cross-platform interoperability instead of closed-loop insurance points

-

Real-time engagement that drivers can actually see and use

-

A modern financial layer purpose-built for transportation

Instead of rewarding drivers with complicated premium calculations hidden inside annual renewals, RideUSD and URT transform incentives into usable transportation value.

Because safer behavior shouldn’t just reduce penalties - it should unlock meaningful rewards drivers can use throughout their everyday mobility experience.

Learn more at Metroblox.io